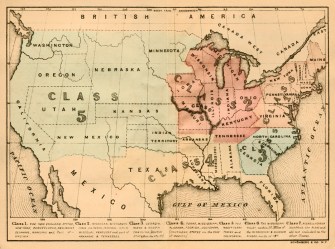

546 – The Underwritten States of America

An apple a day keeps the doctor away. But eating that apple is not enough. Where you eat it matters almost as much. At least it did in the mid-19th century, as demonstrated by these two maps.

They show the territory of the United States divided, for the purpose of medical insurance underwriting, into zones with different levels of ‘safety’. Clearly, the insurance companies considered the area of residence a relevant factor in calculating the risk that the policy would need to be paid out.

The first map, dating from 1855, divides the states and territories of the time into six classes:

- Class 1: Table rates. The most risk-free area of the continental US seemed to be all the states and territories in the northwest, up to the 100th meridian, and above the 40th parallel. That line travels due east until it crossed the Missouri river, after which it follows the river across the eponymous state. At its confluence with the Mississippi, the line stays well east of the river, eventually finding the southern Tennessee border to travel further east, skirting Georgia and taking in the extreme north of South Carolina, finally to bend north and east again, splitting North Carolina in half.

- Class 2: 1/2 per ct. extra for acclimated persons; 2 per ct. extra for unacclimated persons. This zone includes the northern three quarters of Georgia, most of South Carolina, the eastern, coastal half of North Carolina, and northern slices of Alabama and Mississippi. Intriguing. Is there a greater risk for diseases related to warmer climates (malaria etc.)?

- Class 3: As per special agreement. This is the area bounded by the 40th parallel, the Missouri and the Mississippi to the north and east. It includes most of Missouri, Arkansas and the Indian Territory (later to become Oklahoma), and half of Kansas Territory (then much more extended to the west than the state later would be). A wedge-shaped bit slicing into the heart of Texas completes this zone. Does the inclusion of two great rivers allude to an elevated risk of water-borne diseases? And what does special agreement actually mean?

- Class 4: 2 per ct. extra for acclimated persons; 5 per ct. extra for unacclimated persons. Whatever risk the insured run in this zone, which covers the area between Class 2 and Class 3 and the Gulf of Mexico (including Florida, Louisiana, and much of Texas, Alabama and Mississippi), it is four times higher than in Class 2 for acclimated persons (and ‘only’ 2.5 times higher for unacclimated persons).

- Class 5: As per special agreement. This zone is bounded by the 100th meridian in the west and the coastal territories of California, Oregon and Washington in the west (the latter two extending further west than the later states). Do the same risk tariffs apply as in Class 3? Are they tailored to subregions, or to specific professional categories?

- Class 6: One per ct. extra for residence, excluding the mines. California and the Pacific Northwest weren’t too bad for your health, as long as you kept out of the mines. Were the miners uninsurable?

This is “a special category based on malaria regions along the Mississippi Valley,” says Mark Teitelbaum, who sent in these maps.