The tech industry leads the way in revolutionizing student loan debt

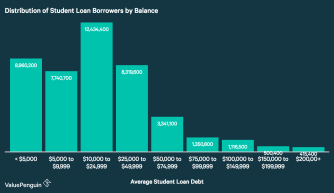

With the average student loan borrower owing in the $27,900—$50,000 range, it’s no wonder that national student loan debt in America is at a record high of $1.52 trillion.

And to make that statistic worse, STEM-based degree programs are pumping out a considerable portion of the borrowers with debt, due to students taking out massive amounts of loans in order to compete in a saturated job market.

A survey shared by CommonBond gave data that depicts how the technology industry might be the most affected the most by student loan debt. Currently, approximately 53% of workers have student loan debts, according to CommonBond, and of those borrows, 65% of them are paying off $50,000 or more in student loans.

Some employers offer student loan repayment as a perk

Initially, innovative startups where the only businesses getting into the student loan repayment assistance game. Now, other industries are using student loan repayment assistance as a way to woo millennials away from the tech industry, targeting those who owe the most – STEM grads.

“Many banks have a rough time attracting millennials as customers, much less as employees,” says Aite Group Senior Analyst Christine Pratt in an interview with American Banker. “But this is a benefit that appeals [to millennials] as something that affects them right at this moment.”

It’s a perk that speaks to career stability says Meera Oliva, Gradifi’s chief marketing officer. Gradifi is a startup that focuses on student loan repayment solutions using machine learning, and was acquired by First Republic Bank in late 2016 after the bank saw huge retainment and hiring successes.

“Tech startups are flush with benefits, but they may not be the most meaningful: things like free beer, snacks, and ping pong tables,” Olivia said. “That’s all good, but it doesn’t have the impact on your life like paying down a student loan. Banks have an opportunity to be a differentiator because this benefit hasn’t really caught on yet in the tech industry.”

In fact, there is only one major tech company that made the Forbes list of the top 10 companies to work for that offer student loan assistance. Nvidia came in at number 6, but there’s a catch: employees are only eligible if they’ve worked there at least three months and have graduated within three years of starting at the company.

Tech is revolutionizing the higher education game

Technology like AI is shaking up the way higher education operates, changing everything from how students search for a college to how they finance it.

The Schoold app allows students to search colleges on any mobile device, allowing them to compare post-graduation salaries by major and school.

Startup Raise.me was able to raise $4.5 million in 2015 and enables students to see which extracurriculars and courses they need to take to be better positioned for scholarships, by using algorithms to match student achievements to micro-scholarships. SaaS platform CampusLogicis using technology to help students complete financial aid more easily by matching students with higher education financial services and financial aid forms.

Startups that are financial aid-related are among the most well-funded startups currently in the market. Many startups are using AI and machine learning to find better ways to provide students with financial aid options. There are even companies that use purely machine-backed data points in their application process.

The higher education industry is turning to tech startups to find a solution for their debt-repayment issues. With the number of federal student loans in default growing, and the number of borrowers owing more than $100,000 growing as well, financial institutions and colleges are looking for a better way to encourage continuing education, without leveraging so much debt against potential students.

Top education technology trends seem to point to student debt loan assistance as a way to carve out differentiators to top job seekers, especially as the federal government and the Trump administration roll back funding for federal financial aid programs.

Student loan repayment, then, seems to be the job perk of the future.